As the world accelerates towards a zero-emissions future, electric vehicles (EVs) are no longer just a niche alternative—they’re becoming mainstream. In New Zealand, EV adoption has surged dramatically. By 2024, 77,670 battery electric vehicles (BEVs) are on the road—a staggering 16-fold increase from just 4,483 in 2017. This growth reflects a strong commitment to sustainability and innovation in transportation.

However, owning an EV isn’t just about being environmentally friendly—it comes with practical considerations like model selection, charging infrastructure, servicing, and, of course, car insurance.

In this post, we’ll explore how insurance for EVs compares to gas vehicles. Factors like repair costs, specialised parts, and advanced technology can all impact premiums. So, does going green mean paying more for car insurance? Let’s take a look.

The EV versus Gas showdown: real insurance comparisons

Using data from the NZ Electric Vehicle Database and Quashed’s Market Scan (which is free to access), we compared three of the most popular EVs with similar petrol and hybrid models. To ensure fairness, we standardised the sum insured, excess, and a driver profile—a 40-year-old from West Auckland. The results below focus solely on comprehensive car insurance.

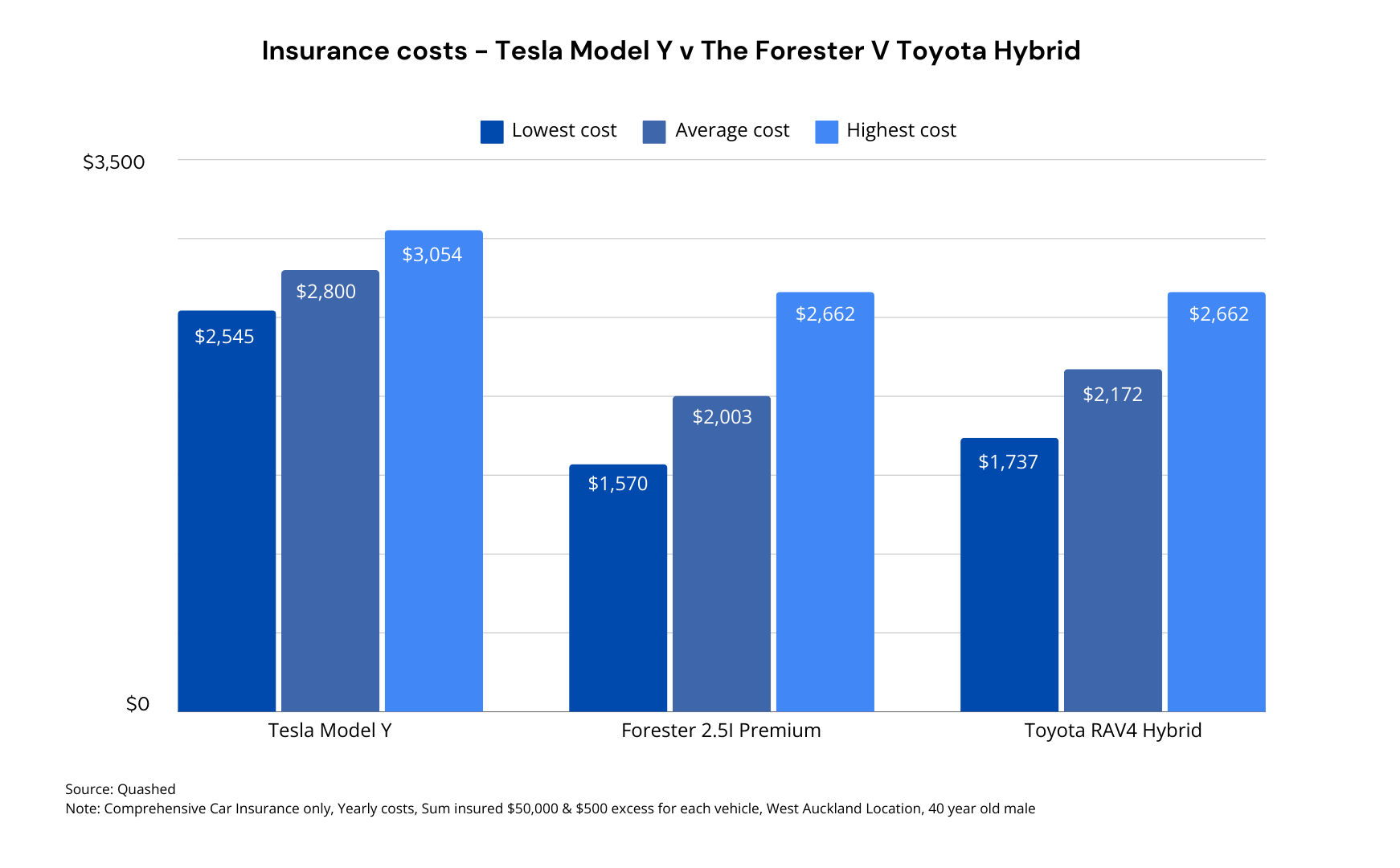

Case study 1: Tesla Model Y v Subaru Forester v Toyota RAV4 Hybrid

In this case study, the Tesla Model Y’s average insurance cost ($2,800) is approximately 40% higher than the petrol Subaru Forester 2.5i ($2,003) and about 29% higher than the Toyota RAV4 Hybrid ($2,172).

So, why the difference? The evidence from around the globe points to several key factors. Tesla vehicles are equipped with advanced technologies, like electric powertrains, which require specialised tools and technicians, often resulting in higher repair costs. Additionally, Tesla, as a newer vehicle manufacturer, lacks the large-scale production and distribution networks that long-established brands like Toyota and Subaru have.

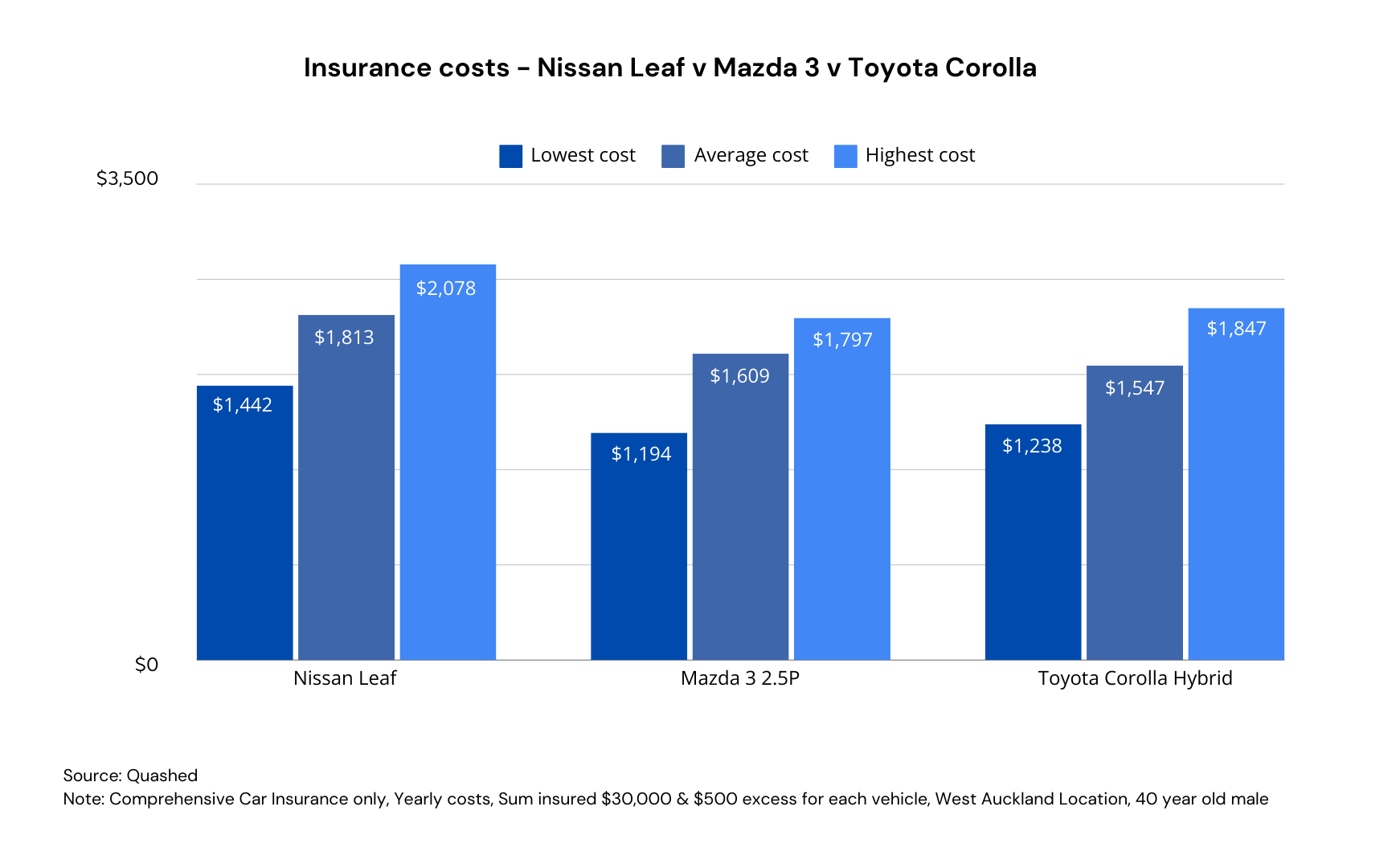

Case study 2: Nissan Leaf v Mazda 3 v Toyota Corolla

In this comparison, the Nissan Leaf stands out with the highest insurance costs, ranging from $1,442 to $2,078, with an average of $1,813. This higher premium reflects the repair complexities common to EVs, particularly the costly battery systems.

Meanwhile, the Toyota Corolla Hybrid offers a solid middle ground, being 15% cheaper to insure than the Leaf. It blends the fuel efficiency of electric technology with the lower insurance costs typical of hybrids, providing a balanced option for cost-conscious drivers.

Although the Corolla Hybrid also outpaces the Mazda 3 in terms of affordability, with a 3.9% reduction in insurance costs, the difference is smaller but still notable, making both the Mazda and the Corolla attractive choices depending on one's preference for hybrid efficiency or traditional petrol.

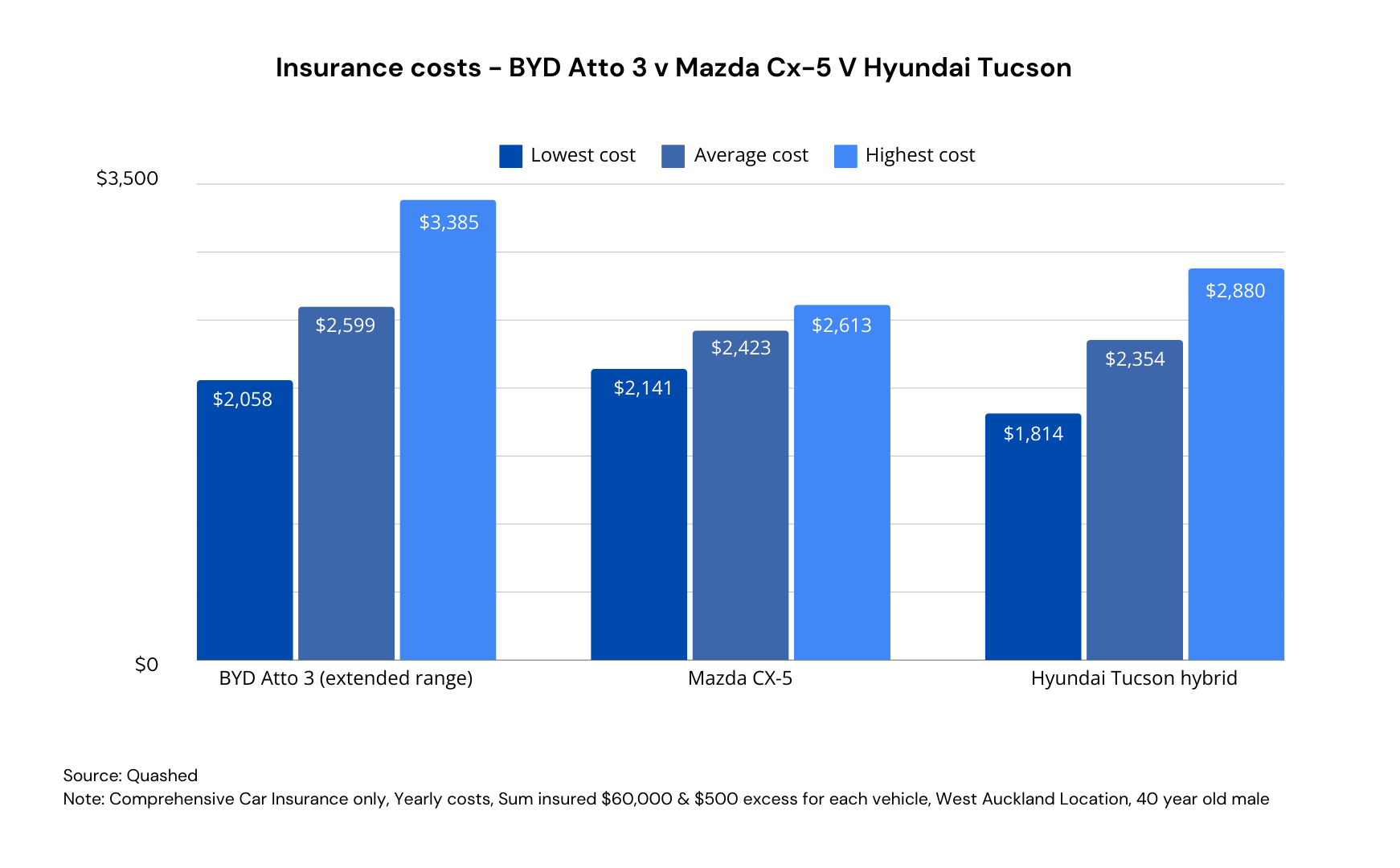

Case study 3: BYD Atto 3 v Mazda CX-5 v Hyundai Tucson

In this case study, the insurance costs for the BYD Atto 3, Mazda CX-5, and Hyundai Tucson Hybrid reveal key insights beyond just technology differences.

The BYD Atto 3, with the highest average cost at $2,599, reflects more than just expensive batteries. Higher premiums stem from specialised repair needs and limited parts availability, making it 7.2% more costly to insure than the Mazda CX-5 and 10.4% more than the Hyundai Tucson Hybrid.

The Mazda CX-5, with an average cost of $2,423, benefits from simpler repairs and a well-established service network. This stability keeps its insurance costs predictable, though still 3.0% higher than the Tucson Hybrid.

The Hyundai Tucson Hybrid, with the lowest average cost of $2,354, strikes a balance between fuel efficiency and lower repair costs. Hybrids, by combining petrol and electric systems, keep premiums down while offering modern technology.

In short, the BYD Atto 3 may be cutting-edge but comes with higher insurance costs due to complex repairs. The Hyundai Tucson Hybrid, meanwhile, offers the best balance of technology and affordability for cost-conscious drivers.

What does this all mean for Kiwi drivers?

For Kiwi drivers, the choice between electric, petrol, or hybrid vehicles isn’t just about fuel efficiency, CO2 emissions, and maintenance costs—it also impacts your insurance premiums.

If you’re considering an electric vehicle like the BYD Atto 3, insurance costs tend to be higher due to expensive repairs and specialised parts, particularly for the battery.

In contrast, petrol vehicles, such as the Mazda CX-5, often provide more predictable and affordable insurance premiums, thanks to simpler repairs and a well-established service network. For drivers prioritising stability in insurance costs, petrol cars remain a reliable choice.

In a previous blog on New Zealand’s most popular vehicles and their insurance costs, we advised Kiwi drivers to consider insurance costs before choosing a car. This advice is especially relevant for car buyers interested in EVs, given their insurance rates can be higher than those for petrol or diesel cars.

What is the future of electric car insurance?

The automotive industry is evolving rapidly. With the rise of EVs, advanced safety technologies, and self-driving features, vehicle insurance is set to undergo significant changes. As technology integrates further into cars, insurance will need to adapt to meet these new demands.

New trends like usage-based insurance, telematics, and risk assessments based on data will likely change vehicle insurance in the future. Let's look at a couple of these trends and predictions more closely.

EV popularity and its impact on insurance

With EVs becoming more common, we can expect more changes in the insurance world to match their new risks and advantages.

In the future, car insurance may involve closer work between car makers, tech providers, and insurance companies. This teamwork will help create new solutions for EV owners.

Tech improvements and better charging options are important for speeding up the use of EVs. These factors will also shape the future of car insurance.

Advances in safety technology and autonomous driving features

Advancements in safety technology, especially in self-driving features, can change car insurance forever. Companies like Tesla and BMW are always working to improve self-driving abilities. Their goal is to make roads safer and reduce mistakes made by drivers.

As these self-driving technologies get better, insurance companies may need to change the way they look at risk and set prices. Switching to self-driving cars will require a major rethink of responsibility when accidents happen. Insurers will create new ways to price and provide coverage.

Though fully self-driving cars are still some years away, features that help drivers today are already impacting insurance prices. Cars with systems like adaptive cruise control, lane-keeping assist, and automatic emergency braking show they have a lower risk of accidents. This could lead to cheaper insurance rates for these vehicles in the future.

How can Quashed help you?

Let's face it—comparing insurance costs for EVs and petrol cars can be a bit of a headache. With so many factors affecting premiums, like repair costs, specialised parts, and where you live, it’s easy to feel overwhelmed.

But that’s where Quashed comes in to make the whole process a lot simpler.

Using our Market Scan, you can quickly compare insurance premiums for different EVs, from the Tesla Model X and Y to the Hyundai Kona Electric.

Here’s how Quashed makes things easier:

See all your options in one place: We bring together quotes from multiple insurance companies, so you can see at a glance who’s offering the best deal—whether you're insuring an EV, hybrid, or petrol car.

Find the cover that suits you: Not all insurance is created equal. We help you understand what each policy covers.

Flexibility: Live in the city? Drive less? Quashed lets you tweak things like your excess to fit your personal situation and get the most accurate quote possible.

Finding EV insurance—fast and easy

Join over 45,000 Kiwis already using Quashed to simplify your insurance.

Don’t wait—sign up for free today, compare quotes, and take the first step towards securing the right EV insurance for you.

Further reading

Smart Ways to Slash Your Car Insurance: Practical tips to reduce your car insurance premiums.

Comparing Insurance Costs for Top Cars in NZ: A comparison of insurance costs across different car models.

Car Insurance for Teslas in New Zealand: A specific look at insuring Teslas, with cost insights and considerations.

Debunking Car Insurance Myths: Common misconceptions about car insurance that could impact your decisions.

Why Is Car Insurance So Expensive?: Factors influencing the high cost of car insurance in NZ.

FAQs

Do EVs really cost more to insure than petrol or diesel cars?

Often, yes—but it depends on the insurer, the model, and the policy. Some EVs come with higher repair costs and pricier parts, and there are fewer specialist repairers in New Zealand. These factors can influence premiums. That said, as EVs become more common, pricing may adjust. Shopping around and comparing policies is the best way to get a competitive rate.

Why are EV repairs more expensive?

EVs include advanced tech and high-cost components, like batteries, that can increase repair costs. Even minor accidents might require specialist work. Insurers factor these risks into pricing, but policies vary—looking for one with comprehensive repair coverage could help in the long run.

Does my EV battery need special insurance?

Most comprehensive policies include battery coverage, but not all policies are the same. If you lease your battery separately, check if it's covered. Some policies exclude gradual battery degradation, so it's worth reading the fine print before committing.

Does charging my EV at home impact my home insurance?

It can. Some insurers ask about EV chargers, as improper wiring may pose a fire risk. If you’re installing one, ensure it’s done professionally and inform your insurer—it helps with transparency and risk assessment.

How can I lower my EV insurance costs?

A few ways:

Opting for a higher excess

Comparing multiple insurers

Choosing an EV-friendly provider

Checking for safe driving discounts or multi-policy deals

Parking in a secure location

Does third-party insurance cover EVs differently?

Nope—third-party policies work the same for EVs as they do for petrol cars. But if your EV is on the pricier side, full cover might be the smarter option to avoid hefty repair bills if something goes wrong.

Are there insurers in NZ that specialise in EVs?

Some insurers offer EV-specific benefits like battery protection and approved repair networks. Not all explicitly specialise, but some policies are more tailored to EV owners. It pays to compare.

Does third-party insurance cover EVs differently?

No—third-party works the same way regardless of fuel type. But if your EV is on the pricier side, full cover may be worth considering to avoid unexpected repair costs.

Will EV insurance get cheaper over time?

It’s possible. As EV adoption increases and repair networks expand, insurers may adjust pricing. However, changes depend on multiple factors, including claims data, repair costs, and market trends. Keeping an eye on the market can help you find the best deal.

This article provides general information only and does not constitute insurance or financial advice. Insurance policies vary between providers, and you should check with your insurer or a licensed adviser for guidance specific to your situation. For full details, refer to Quashed’s terms and conditions.